Despite the significant rebound in US equities since the announcement of a cease-fire — particularly the surge in mega cap technology stocks — we believe the conditions that underpinned the earlier change in market sentiment remain largely in place.

While we cannot know for sure, we suspect that given these cross currents, the recent surge in market volatility may not yet have run its course. In such an environment, we are reassured by our Funds’ attractive valuations.

Tweedy, Browne Funds Commentary, Q1 2026The seemingly indefatigable US technology led advance in global equity markets over the last few years faced macroeconomic headwinds in the first quarter, as global equity markets experienced a decline. Heightened geopolitical tensions, including military conflict involving Iran and the resulting disruption to global oil supply, contributed to increased volatility and a general sense of unease among investors.

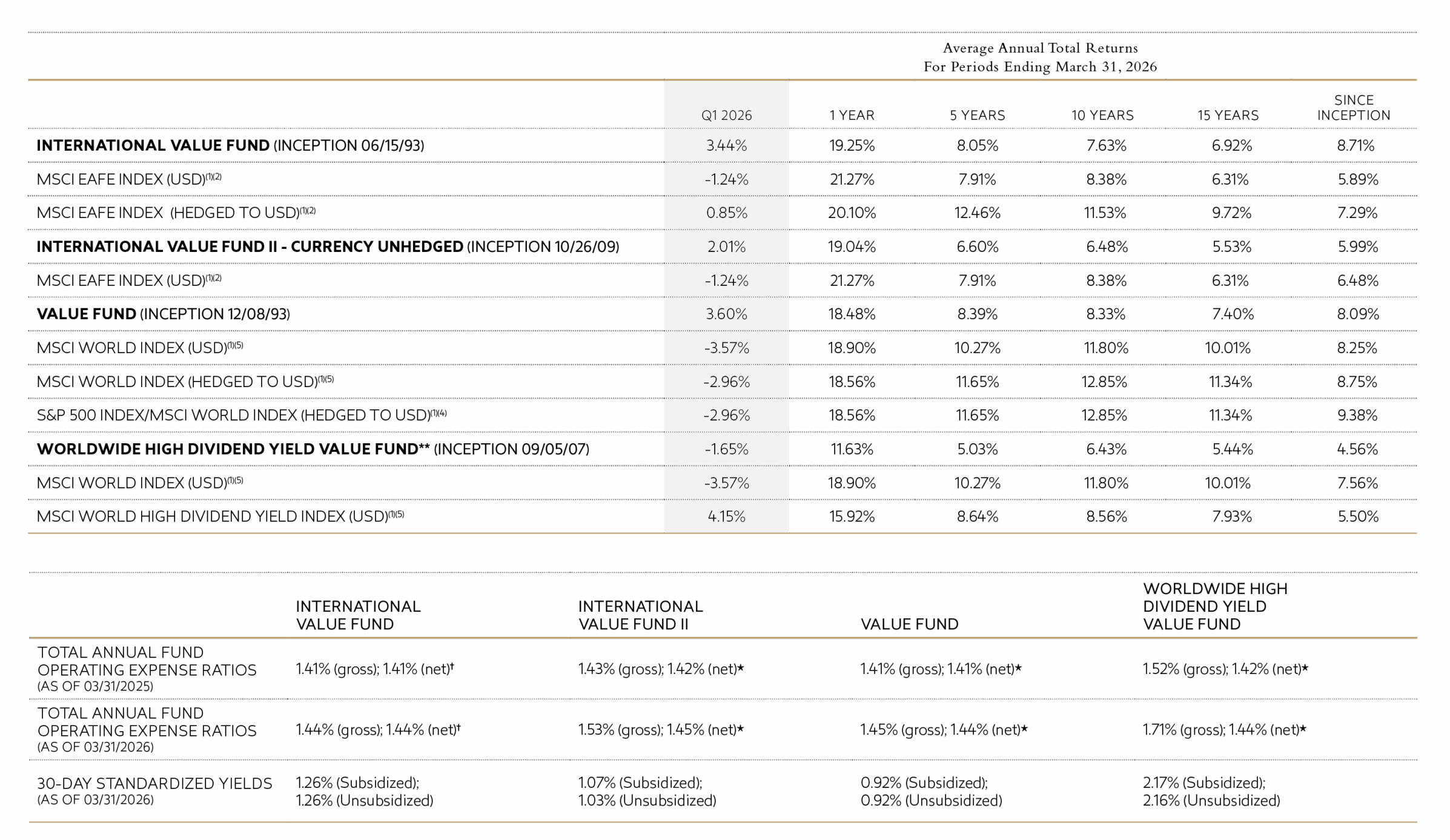

Concerns about potential interruptions in the future supply of oil, coupled with a spike in oil prices in March, dampened somewhat the recent outperformance of non-US equities relative to their US counterparts. Nevertheless, the performance of non-US equity markets, as represented by the MSCI EAFE Index, still outperformed US equities for the 1st quarter, and for the 12 months ending March 31.

The performance data shown above represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Please visit www.tweedyfunds.com to obtain performance data which is current to the most recent month end.

† Tweedy, Browne has voluntarily agreed, effective May 22, 2020 through at least July 31, 2026, to waive the International Value Fund’s fees whenever the Fund’s average daily net assets (“ADNA”) exceed $6 billion. Under the arrangement, the advisory fee payable by the Fund is as follows: 1.25% on the first $6 billion of the Fund’s ADNA; 0.80% on the next $1 billion of the Fund’s ADNA (ADNA over $6 billion up to $7 billion); 0.70% on the next $1 billion of the Fund’s ADNA (ADNA over $7 billion up to $8 billion); and 0.60% on the remaining amount, if any, of the Fund’s ADNA (ADNA over $8 billion). The performance data shown above would have been lower had fees not been waived during certain periods. The Adviser has agreed to waive the Fund’s management fee to the extent of any management fee charged in connection with the portfolio of the Fund’s assets that are allocated to an Affiliated Fund (as defined in the Fund’s Prospectus). Such waiver shall continue until January 31, 2027.

* Tweedy, Browne has voluntarily agreed, effective December 1, 2017 through at least July 31, 2026, to waive a portion of the International Value Fund II’s, the Value Fund’s and the Worldwide High Dividend Yield Value Fund’s investment advisory fees and/or reimburse a portion of each Fund’s expenses to the extent necessary to keep each Fund’s expense ratio in line with the expense ratio of the International Value Fund. (For purposes of this calculation, each Fund’s acquired fund fees and expenses, brokerage costs, interest, taxes and extraordinary expenses are disregarded, and each Fund’s expense ratio is rounded to two decimal points) The net expense ratios set forth above reflect this limitation, while the gross expense ratios do not. The International Value Fund II’s, Value Fund’s and Worldwide High Dividend Yield Value Fund’s performance data shown above would have been lower had fees and expenses not been waived and/or reimbursed during certain periods.

** Effective May 27, the Tweedy, Browne Worldwide High Dividend Yield Value Fund will be renamed the Tweedy, Browne . Buybacks . Dividends + Value Fund.

The Funds do not impose any front-end or deferred sales charges. The expense ratios shown above reflect the inclusion of acquired fund fees and expenses (i.e., fees charged by the Adviser on Affiliated Funds and the fees/expenses attributable to investing cash balances in money market funds) and may differ from those shown in the Funds’ financial statements.

As we write in early May, a fragile cease-fire in the Iranian conflict has helped to spark a rebound in global equity indices, led by an unusually robust rally in US-based high technology companies. It remains to be seen whether market sentiment will eventually revert to the AI-related market concerns that had emerged prior to the outbreak of hostilities.

Against that backdrop, all four Funds outperformed their benchmarks for the quarter, with three of the four posting positive absolute returns. The International Value Fund returned 3.44%, ahead of its primary benchmark, the MSCI EAFE Index (in USD) which declined by 1.24%, and the MSCI EAFE Index hedged to USD which rose 0.85%. The International Value Fund II gained 2.01%, outperforming the MSCI EAFE Index (in USD), which declined 1.24%. The Value Fund returned 3.60%, well ahead of the MSCI World Index in USD and the MSCI World Index (Hedged to USD), which fell 3.57% and 2.96%, respectively. The Worldwide High Dividend Yield Value Fund declined 1.65%, but nonetheless outperformed its benchmark, the MSCI World Index (in USD), which was down 3.57%.

*The performance data shown above represents past performance and is not a guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Please visit www.tweedyfunds.com to obtain performance data which is current to the most recent month end.

Despite the significant rebound in US equities since the announcement of a cease-fire — particularly the surge in mega cap technology stocks — we believe the conditions that underpinned the earlier change in market sentiment remain largely in place.

Please note that the individual companies discussed herein were held in one or more of the Funds during the quarter ended March 31, 2026, but were not necessarily held in all four of the Funds. Please refer to the full commentary (beginning of page 6) for selected purchase and sale information during the quarter and the notes on page 15 for each Fund’s respective holdings in each of these companies as of March 31, 2026.

In terms of portfolio attribution during the quarter, aside from the Worldwide High Dividend Yield Value Fund, from a sector perspective, Energy and Materials were among the Funds’ most significant contributors. Strength in oil and gas holdings, particularly TotalEnergies, provided a meaningful tailwind, while exposure to chemicals and related businesses benefited from a somewhat improved outlook for cyclical end markets. Within Information Technology, contributions were more selective but important, with semiconductor-related holdings such as Samsung Electronics contributing positively.

Industrials also added to returns in aggregate, with contributions spread across a number of industries, including machinery, aerospace and defense, and distribution businesses. Companies such as CNH Industrial (agricultural equipment) and BAE Systems (defense) were notable contributors and reflect durable competitive positions and increasing demand. Health Care holdings were more mixed, with gains in some large pharmaceutical holdings offset by weakness in other areas.

By contrast, Consumer Discretionary was a source of weakness. Holdings tied to consumer demand, including automotive-related companies and certain service businesses, detracted from results as economic momentum appeared uneven. Consumer Staples and Communication Services also detracted, with certain service-oriented businesses facing continued operational and AI sentiment-related challenges.

From a geographic standpoint, South Korea and France were among the more significant contributors, supported by strong performance in holdings such as Samsung Electronics and TotalEnergies. Japan also contributed positively in local currency terms. In contrast, Germany, Sweden, and China detracted from returns, reflecting weaker performance in industrial and consumer-facing businesses.

At the individual security level, a relatively small number of holdings accounted for a meaningful portion of returns. TotalEnergies, Samsung Electronics, CNH Industrial, Roche, Novartis, and BAE Systems were among the more significant contributors. Detractors were more dispersed and included a number of consumer-facing and service-oriented businesses, as well as select health care holdings.

In the Worldwide High Dividend Yield Value Fund, Health Care and Communication Services were the top contributing sectors. This included strong performance from the Fund’s pharma holdings Roche and Novartis, as well as Megacable, the Mexican provider of internet, phone, and cable services. Switzerland and Mexico were the top contributing countries, due to the performance of those same three stocks. Other top performing stocks included Bunzl, CNH Industrial, Rubis, Aalberts, and United Overseas Bank.

In contrast, the Fund’s Consumer Discretionary holdings were a source of weakness, including a few auto-related holdings such as Subaru, Isuzu Motors, Autoliv, and Inchcape. Japan, France, and Sweden were the largest detracting countries, with negative returns from Subaru, Teleperformance, and Safran, among others. The top individual detractors also included Diageo, Zurich Insurance, and Breedon Group.

Currency movements were a modest headwind during the quarter. The US dollar strengthened against most major currencies, including the euro, British pound, Japanese yen, and Swiss franc, with more pronounced declines in the South Korean won and Swedish krona. As expected, the currency hedged Funds were largely insulated from these effects, while the unhedged Funds experienced some negative translation impact.

A list of selected newly established positions, including additions, sales, and trims of existing positions for each Fund, is included in the full commentary, beginning on page 6.

Portfolio activity during the quarter in large part involved trimming or exiting positions where the valuation gap between original cost and intrinsic value had narrowed and reallocating capital toward what we believe are more attractively valued businesses

We established several new positions across the Funds during the quarter. Among the more notable were Autotrader, Bunzl, and Springer Nature , each of which, we believe were trading at purchase at a significant discount to their respective intrinsic values, are financially strong, and have runways of future growth. We also took advantage of pricing opportunities, and added to our positions in Vetropack, CVS Group, Sodexo, Sysmex, Johnson Service, and Breedon Group.

On the sales side, we exited a number of positions in the International Value Fund, including Niterra, Sopra Steria, Mitsubishi Gas, and Howden Joinery, as well as Takara Holdings and Kanadevia in other Fund portfolios. These decisions were generally driven by valuation considerations, and the opportunity to redeploy capital into more compelling opportunities. In some instances, we trimmed or sold positions to recognize tax losses.

In addition, we trimmed back a number of positions during the quarter that had appreciated and were approaching our estimates of underlying intrinsic value. These included holdings such as TotalEnergies, Samsung Electronics, BAE Systems, Roche, and Novartis. While we continue to view these as desirable portfolio holdings, we believe it is prudent to trim position sizes and recycle capital as valuations evolve. We also reduced our position in Diageo in light of valuation considerations and the near-term challenges it faces from changes in drinking patterns and GLP-1 weight loss drugs.

ETF share classes. As we reported last quarter, our application for exemptive relief to establish ETF share classes for our Funds was approved by the S.E.C. and we are continuing to explore this initiative. We are excited about the opportunity to offer our shareholders a choice when investing in our funds, and we will continue to keep you apprised of our progress.

Change of name/strategy in the Worldwide High Dividend Value Fund. Since its inception, the Worldwide High Dividend Yield Value Fund’s (TBHDX) investment approach has focused on investment in companies around the world that had an above average dividend yield and that traded at reasonable valuations. While an above average yield was an important component of the approach as it was often an indicator of financial strength and undervaluation, generating income was never our focus, and was simply a by-product of our approach. Attractive shareholder yields, as evidenced in part, by a company’s willingness to buyback shares when their shares appeared to be undervalued, or to pay down debt were an additional, but secondary component of our approach.

As of May 27, 2026, the Fund’s investment strategy will be modestly adjusted to emphasize investment in companies that pay an attractive dividend and/or have initiated buybacks of their shares, when those shares are trading at discounts to underlying value — including undervaluation based on proprietary combinations of various numerical investment characteristics, a value score, and qualitative assessments. The Fund will no longer require an above average dividend. This focus on the dividend and/or buyback components of shareholder yield coupled with undervaluation is consistent with a change in the Fund’s name to the Tweedy, Browne . Buybacks . Dividends + Value Fund. The impetus for this modest change in strategy was proprietary empirical work evidencing a return advantage over time for stocks trading at significant discounts to conservative estimates of intrinsic value where the company was engaged in buying back its shares in the open market and ultimately retiring them. We are excited about this modest change in focus, and what it could mean for the future prospects of our Fund. Should you have any questions or concerns regarding this adjustment in the Fund’s strategy, please do not hesitate to reach out. Click here to see the supplement that was filed with the US Securities and Exchange Commission on March 27, 2026, for more details.

We have been encouraged over the last year by the resurgence in value-oriented equities, particularly among smaller and medium capitalization non-US equities. Prior to the outbreak of hostilities, the proverbial “puck” genuinely appeared to be coming our way, reflecting in our view a long overdue sea change in equity market leadership. Despite the significant rebound in US equities since the announcement of a cease-fire – particularly the surge in mega cap technology stocks – we believe the conditions that underpinned the earlier change in market sentiment remain largely in place.

While we cannot know for sure, we suspect that given these cross currents, the recent surge in market volatility may not yet have run its course. In such an environment, we are reassured by our Funds’ attractive valuations.

We remain humbled by your investment in our Funds and thank you for your continued trust and confidence.

Roger R. de Bree, Andrew Ewert, Frank H. Hawrylak, Jay Hill, Thomas H. Shrager, John D. Spears, Robert Q. Wyckoff, Jr. | Investment Committee* | Tweedy, Browne Company LLC

April 2026

* Each member of the Investment Committee is a current investor in one or more of the Funds.

NOTES

(1) Indexes are unmanaged, and the figures for the indexes shown include reinvestment of dividends and capital gains distributions and do not reflect any fees or expenses. Investors cannot invest directly in an index.

(2) The MSCI EAFE Index is a free float-adjusted, market capitalization weighted index that is designed to measure the equity market performance of developed markets, excluding the US and Canada. The MSCI EAFE Index (in USD) reflects the return of the MSCI EAFE Index for a US dollar investor. The MSCI EAFE Index (Hedged to USD) consists of the results of the MSCI EAFE Index hedged 100% back into US dollars and accounts for interest rate differentials in forward currency exchange rates. Results for each index are inclusive of dividends and net of foreign withholding taxes.

(3) Inception dates for the International Value Fund, International Value Fund II, Value Fund and Worldwide High Dividend Yield Value Fund are June 15, 1993, October 26, 2009, December 8, 1993, and September 5, 2007, respectively. Prior to 2004, information with respect to the MSCI EAFE and MSCI World Indexes used was available at month end only; therefore, the since-inception performance of the MSCI EAFE Indexes quoted for the International Value Fund reflects performance from May 31, 1993, the closest month end to the International Value Fund’s inception date, and the since inception performance of the MSCI World Index quoted for the Value Fund reflects performance from November 30, 1993, the closest month end to the Value Fund’s inception date. For International Value Fund, information with respect to the Morningstar Foreign Stock Fund Average or the Foreign Stock Fund Average (see note 6 below) are available at month end only; therefore, the closest month end to the inception date of the International Value Fund, May 31, 1993, was used.

(4) The S&P 500/MSCI World Index (Hedged to USD) is a combination of the S&P 500 Index and the MSCI World Index (Hedged to USD), linked together by Tweedy, Browne, and represents the performance of the S&P 500 Index for the periods 12/08/93 – 12/31/06 and the performance of the MSCI World Index (Hedged to USD) beginning 01/01/07 and thereafter (beginning December 2006, the Fund was permitted to invest more significantly in non-US securities). The S&P 500 Index is a market capitalization weighted index composed of 500 widely held common stocks that assumes the reinvestment of dividends. The index is generally considered representative of US large capitalization stocks.

(5) The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index (in USD) reflects the return of this index for a US dollar investor. The MSCI World Index (Hedged to USD) consists of the results of the MSCI World Index with its foreign currency exposure hedged 100% back into US dollars. The index accounts for interest rate differentials in forward currency exchange rates. The MSCI World High Dividend Yield Index reflects the performance of equities in the MSCI World Index (excluding REITs) with higher dividend income and quality characteristics than average dividend yields that are both sustainable and persistent. The index also applies quality screens and reviews 12-month past performance to omit stocks with potentially deteriorating fundamentals that could force them to cut or reduce dividends. The MSCI World High Dividend Yield Index (in USD) reflects the return of the MSCI World High Dividend Yield Index for a US dollar investor. Results for each index are inclusive of dividends and net of foreign withholding taxes.

(6) Since September 30, 2003, the Foreign Stock Fund Average is calculated by Tweedy, Browne based on data provided by Morningstar and reflects average returns or portfolio turnover rates of all mutual funds in the Morningstar Foreign Large-Value, Foreign Large-Blend, Foreign Large-Growth, Foreign Small/Mid-Value, Foreign Small/Mid-Blend, and Foreign Small/Mid-Growth categories. Funds in these categories typically invest in international stocks and devote no more than 20% of assets to US equity markets. These funds may or may not be hedged to the US dollar, which will affect reported returns. References to “Foreign Stock Funds” or the “Foreign Stock Fund Average” that predate September 30, 2003 are references to Morningstar’s Foreign Stock Funds and Foreign Stock Fund Average, respectively, while references to Foreign Stock Funds and the Foreign Stock Fund Average for the period beginning September 30, 2003 refer to Foreign Stock Funds and the Foreign Stock Fund Average as calculated by Tweedy, Browne.

(7) Since April 28, 2017, the Global Stock Fund Average is calculated by Tweedy, Browne based on data provided by Morningstar, and reflects average returns or portfolio turnover rates of all mutual funds in the Morningstar Global Large Stock (including Global Large Value, Global Large Growth, and Global Large Blend categories) and Global Small/Mid Stock categories. Prior to April 28, 2017, the Global Stock Fund Average was calculated by Morningstar. Funds in these categories typically invest in stocks throughout the world while maintaining a percentage of their assets (normally 20% – 60%) invested in US stocks. These funds may or may not be hedged to the US dollar, which will affect reported returns. References to “Global Stock Funds” or the “Global Stock Fund Average” that predate April 28, 2017 are references to Morningstar’s Global Stock Funds and Global Stock Fund Average, respectively, while references to Global Stock Funds and the Global Stock Fund Average for the period beginning April 28, 2018 refer to the Global Stock Funds and Global Stock Fund Average as calculated by Tweedy, Browne.

The Funds are actively managed, unlike the indexes, and consist of securities that vary widely from those included in the indexes in terms of portfolio composition, country and sector allocations, and other metrics. Hedged indexes are included to illustrate how the stocks that are components of the hedged indexes would have performed in their local currencies for a US dollar investor. The hedged indexes are fully nominally hedged on a monthly basis, whereas the International Value Fund and the Value Fund hedge their perceived currency exposure only where practicable. Tweedy, Browne applies a different hedging methodology than the hedged indexes. Index results are shown for illustrative purposes only.

The performance results reflected above are over the course of many years and reflect multiple market cycles and varying geopolitical, market and economic conditions. Past performance is no guarantee of future results.

DEFINITIONS

The Buffett Indicator, also known as the Market Capitalization-to-GDP ratio, is a valuation metric that assesses the price of the stock market relative to a country’s GDP. It’s calculated by dividing the total market value of a country’s publicly-traded stocks by its GDP.

The Shiller CAPE Index, also known as the cyclically adjusted price-to-earnings ratio, is a stock valuation metric that compares a stock’s current price to its average inflation-adjusted earnings over the previous 10 years. The CAPE index is used to assess whether a stock or market is overvalued or undervalued, and to forecast future returns.

Content reproduced from Morningstar is ©2026 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

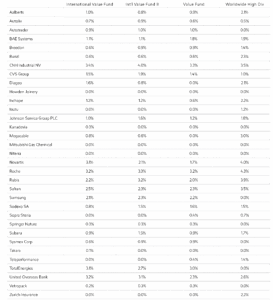

As of March 31, 2026, the International Value Fund, International Value Fund II, Value Fund, and Worldwide High Dividend Yield Value Fund had each invested the following percentages of its net assets, respectively, in the following portfolio holdings:

The above listed portfolio holdings reflect the Funds’ investments on the date indicated and may not be representative of the Funds’ current or future holdings. Selected Purchases & Sales illustrate some or all of the largest purchases and sales made for each Fund during the preceding quarter and may not include all purchases and sales. Some “undisclosed” names may have been withheld where disclosure may be disadvantageous to a Fund’s accumulation or disposition program.

All investing involves the risk of loss, including the loss of principal. Current and future portfolio holdings are subject to risk. The securities of small, less well-known companies may be more volatile than those of larger companies. In addition, investing in foreign securities involves additional risks beyond the risks of investing in securities of US markets. These risks which are more pronounced in emerging markets, include economic and political considerations not typically found in US markets, including currency fluctuation, political uncertainty and different financial standards, regulatory environments, and overall market and economic factors. Force majeure events such as pandemics and natural disasters are likely to increase the risks inherent in investments and could have a broad negative impact on the world economy and business activity in general. Value investing involves the risk that the market will not recognize a security’s intrinsic value for a long time, or that a security thought to be undervalued may in fact be appropriately priced when purchased. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Diversification does not guarantee a profit or protect against a loss in declining markets.

Although the practice of hedging perceived foreign currency exposure, where practicable, utilized by the International Value Fund and Value Fund reduces the risk of loss from exchange rate movements, it also reduces the ability of the Funds to gain from favorable exchange rate movements when the US dollar declines against the currencies in which the Funds’ investments are denominated and may impose costs on the Funds. As a result of practical considerations, fluctuations in a security’s prices, and fluctuations in currencies, a Fund’s hedges are expected to approximate, but will generally not equal, the Fund’s perceived foreign currency risk.

Stocks and bonds are subject to different risks. In general, stocks are subject to greater price fluctuations and volatility than bonds and can decline significantly in value in response to adverse issuer, political, regulatory, market or economic developments. Unlike stocks, if held to maturity, bonds generally offer to pay both a fixed rate of return and a fixed principal value. Bonds are subject to interest rate risk (as interest rates rise bond prices generally fall), the risk of issuer default, issuer credit risk, and inflation risk, although US Treasuries are backed by the full faith and credit of the US government.

Investors should refer to the prospectus for a description of risk factors associated with investments in securities which may be held by the Funds. Investing involves the risk of loss, including the loss of principal. There is no assurance that a Fund will achieve its investment objective.

This commentary contains opinions and statements on investment techniques, economics, market conditions and other matters. There is no guarantee that these opinions and statements will prove to be correct, and some of them are inherently speculative. None of them should be relied upon as statements of fact. The views expressed herein represent the opinions of Tweedy, Browne Company LLC as of the date of this commentary, are not intended as a forecast or a guarantee of future results, or investment advice and are subject to change without notice.

Tweedy, Browne International Value Fund, Tweedy, Browne International Value Fund II – Currency Unhedged, Tweedy, Browne Value Fund, and Tweedy, Browne Worldwide High Dividend Yield Value Fund are distributed by AMG Distributors, Inc., Member FINRA/SIPC.

This material must be preceded or accompanied by a current prospectus for Tweedy, Browne Fund Inc. Click here for a copy of the Funds’ prospectus. You should consider the Funds’ investment objectives, risks, charges and expenses carefully before investing. The prospectus contains this and other information about the Funds. The prospectus should be read carefully before investing.

You are navigating from Tweedy U.S. Funds to {{ TARGET_SITE }}.